By John I. Adams, Chairman, TSCL

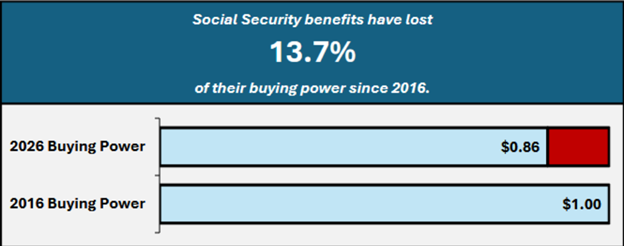

Last month, TSCL published the latest edition of its long-running Loss of Buying Power studies. This research (available for free) suggests that Social Security benefits in 2026 are only worth about 83.6 cents on the dollar compared to their 2016 value. The study estimates that benefits have lost 13.7 percent of their buying power due to Cost-of-Living Adjustments (COLAs) that do not keep up with real-world inflation.

These findings corroborate what seniors like you already tell us: They’re under immense financial pressure! Our previous research has found that 79 percent of seniors believe inflation substantially outpaced the COLA in 2024, while 39 percent depend on Social Security for all of their income.

Insufficient COLAs, even small misses against inflation, quickly add up for seniors who depend on their benefits to get by. The 2026 Loss of Buying Power estimates that, for the average senior shopping as affordably as possible, overall inflation since 2016 comes out to about 43.55 percent, while the government figure used to calculate the COLAs (the CPI-W) measures 10-year inflation at 37.60 percent.

How Did TSCL Get Its Loss of Buying Power Number for 2026?

TSCL built its own proprietary dataset for this study. Primarily using a tool called the Wayback Machine, which acts like a time machine for the internet, we compiled historical prices for 70 products and services for 2016 and 2026. Then, we calculated the percentage change, making sure to weight different expense categories (such as housing and transportation) so they make up the right proportion of a typical budget when calculating inflation. We then compared our figure to the CPI-W’s 10-year inflation figure.

You can find a detailed description of how we built our dataset (including all our sources) in the study’s methodology section. However, the most important detail to note is that we built our index as if we were shopping affordably. We asked ourselves, “How would a senior living on only Social Security shop?” as a guiding question when selecting data to include in the index.

Which Prices Rose the Most From 2016 to 2026?

Among the 70 items in the 2026 Loss of Buying Power Index, housing and transportation costs rose the most in total value since 2016. Homes, new cars, used cars, vehicle ownership costs (including fuel, insurance, and maintenance), and rent all made the top 10. Of these, the only item whose price didn’t rise at a faster rate than overall inflation was the average used car price.

What Does Social Security’s Lost Buying Power Mean for Retirees?

In two words, economic distress. TSCL’s study estimates that benefits would need to rise by 15.7 percent across the board to make up for the purchasing power they’ve lost over the last decade. For the average Social Security beneficiary to get the same value from their benefits today as they did in 2016, we project that the monthly checks would need to increase by $295.85 per month, or about $3,550.20 annually.

How Can Seniors Recover Their Lost Benefits?

This one is going to take an act of Congress. To bring benefits back into line with their historic purchasing power, Congress would need to approve a one-time increase of 15.7 percent to monthly checks. However, this would only rectify the situation for future payments, not make up the lost value for seniors who’ve watched their benefits steadily erode for years.

TSCL calls for Congress to issue seniors a raise on current benefits, then issue a one-time stimulus of $3,550.20 for all Social Security beneficiaries to at least partially refund people for years of lagging COLAs. Next, to fund these improved benefits, TSCL advocates for what our research identified as seniors’ favorite way to strengthen Social Security’s finances: Eliminating the tax loophole that lets people stop paying payroll taxes into Social Security on income above $184,500.

If you’d like to get involved, visit our website’s Action Center. Here, you can sign our petitions for Congress, participate in the surveys we use to collect data for our policy research, and make toll-free calls to your Representative and Senators to express your support for strengthening Social Security for today’s and tomorrow’s Americans.