By Alex Moore

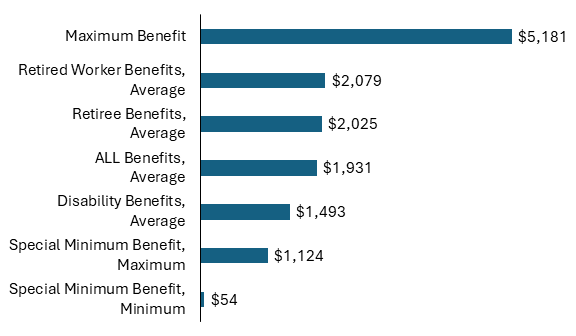

As of March 2026, the latest month with data available as this article goes to press, the average Social Security benefit was $1,931.05. That’s across all types of beneficiaries, regardless of how much they earned during their working years. However, not all Social Security benefits are created equally. As shown in the chart below, monthly payments in 2026 can range from as little as $54 per month to $5,181.

Average Monthly Social Security Payments in 2026

Why Do Some People Earn More in Social Security Benefits Than Others?

Long story short? People who earn more during their careers bring in more benefits.

Social Security determines how much a person will earn in retirement benefits using a complicated formula. The formula considers how long you worked, how much you made, inflation, and when you started claiming your benefits. Social Security looks at your earnings during the 35 best-paid years of your career, adjusts them for inflation to today’s dollars, and takes the average. That number feeds into another formula, which Social Security uses to determine your starting benefit amount, which is again modified with a penalty for people who retire before 65 and a bonus for those who wait to retire.

Years of your adulthood when you had no income can hurt you in the formula. If you have less than 35 years of work history, the formula counts any years you did not work as zeroes, lowering your average income.

How Could Social Security Pay Someone Just $54 a Month?

Social Security has provided what’s called the Special Minimum Benefit for low-income workers, or people with substantial work history but very low earnings, since 1972. It is calculated based on how many years you worked rather than how much you earned. Few people take the Special Minimum benefit today because most low-income earners would earn more using the standard formula.

The lowest possible monthly payment for people on the Special Minimum benefit of just $54 is for those with only 11 years of work experience who accepted a 30 percent benefits penalty to retire at 62, the first year in which Americans become eligible. The highest possible payment for the Special Minimum Benefit in 2026 is $1,124, for people who worked at least 30 years and waited until age 70 to retire.

What Would It Take to Bring in $5,181 in Benefits?

The maximum Social Security benefit is the absolute most that the SSA will pay any beneficiary in any given month. The maximum benefit exists because there’s a cap on how much of your earnings are subject to Social Security payroll taxes, which the SSA updates every year. (The cap in 2026 is $184,500.) This means that the government effectively limits the maximum you can pay into the program over your career but also limits the maximum you can earn from it.

To earn the maximum benefit, you need to meet three criteria:

- You need to earn more than the income cap for Social Security payroll taxes in 35 consecutive years (in 2026, that would be $184,501).

- You must wait until age 70 to claim your retirement benefits. Your benefits increase by 8 percent per year for each year you wait from full retirement age (67 for someone born after 1960) until age 70.

- You must be born in the right year. The baseline used to calculate your benefits changes with every birth year, with the cohort turning 70 this year being eligible for the highest amount.

These criteria are very difficult to meet, making it very rare for someone to earn the maximum Social Security benefit. Only about 6 percent of American workers in any one year earn enough to hit the cap on Social Security taxes, let alone accomplishing it for 35 years.

How Can You Maximize Your Benefits?

If you haven’t claimed your Social Security benefits, it may be a good idea to wait if you can afford it and have not turned 70 yet. As mentioned earlier in this article, you can face up to a 30 percent penalty on your benefits if you claim your retirement benefits as soon as you’re eligible at age 62. In comparison, you will bring in an additional 8 percent of benefits every year for every year you wait to claim between full retirement age and 70 years old.

If you’re already retired and need help, TSCL recommends looking for public assistance. The truth is, our research shows seniors feel like they’re falling behind financially, with 44 percent relying on at least one public assistance program to get by. Asking for help is never fun, but USA.gov has a tool that can help you find programs you may qualify for.

In the meantime, we at TSCL will keep fighting for you. Funded only by public donations, no government or corporate money, we push Congress to reform Social Security’s finances, increase benefits through stronger Cost-of-Living Adjustments (COLAs), expand Medicare coverage, and more. You can learn more about our advocacy efforts here.