For Immediate Release – October 15th, 2025

The cost of using the wrong price index is rising for seniors over time. As shown in the figure below, TSCL’s analysis predicts that, if current long-term inflation patterns continue, the average person who retired in 2014 will lose about $8,000 of benefits across a 25-year retirement from using COLAs calculated with the CPI-W instead of the CPI-E. For someone who retired in 2024, we project that number to rise to just over $12,000.

Key Insights:

The cost of using the wrong price index is rising for seniors over time. As shown in the figure below, TSCL’s analysis predicts that, if current long-term inflation patterns continue, the average person who retired in 2014 will lose about $8,000 of benefits across a 25-year retirement from using COLAs calculated with the CPI-W instead of the CPI-E. For someone who retired in 2024, we project that number to rise to just over $12,000.

Key Insights:

As COLA Announcement Delayed, Seniors Miss Out on Thousands of Dollars in Social Security Payments Due to Bad Government Policy

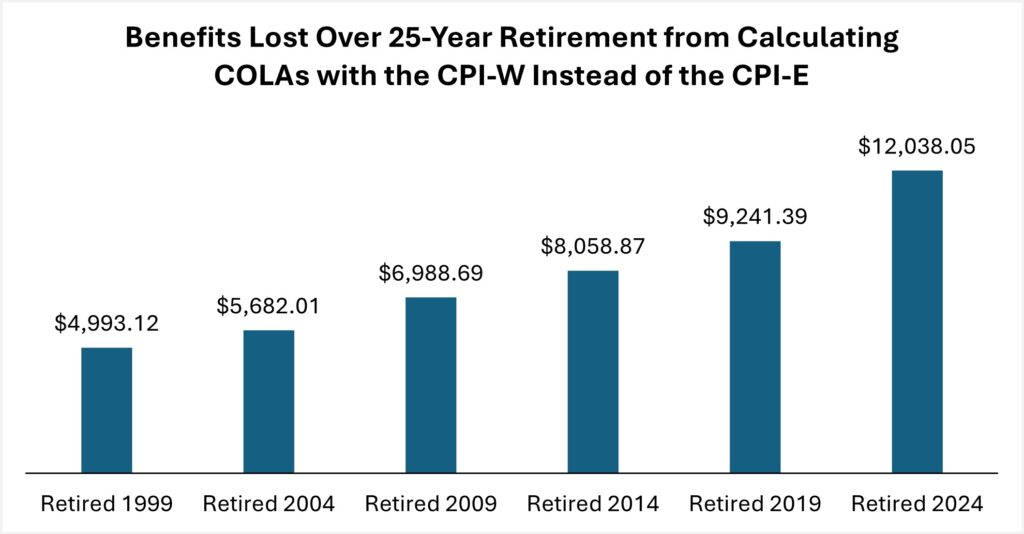

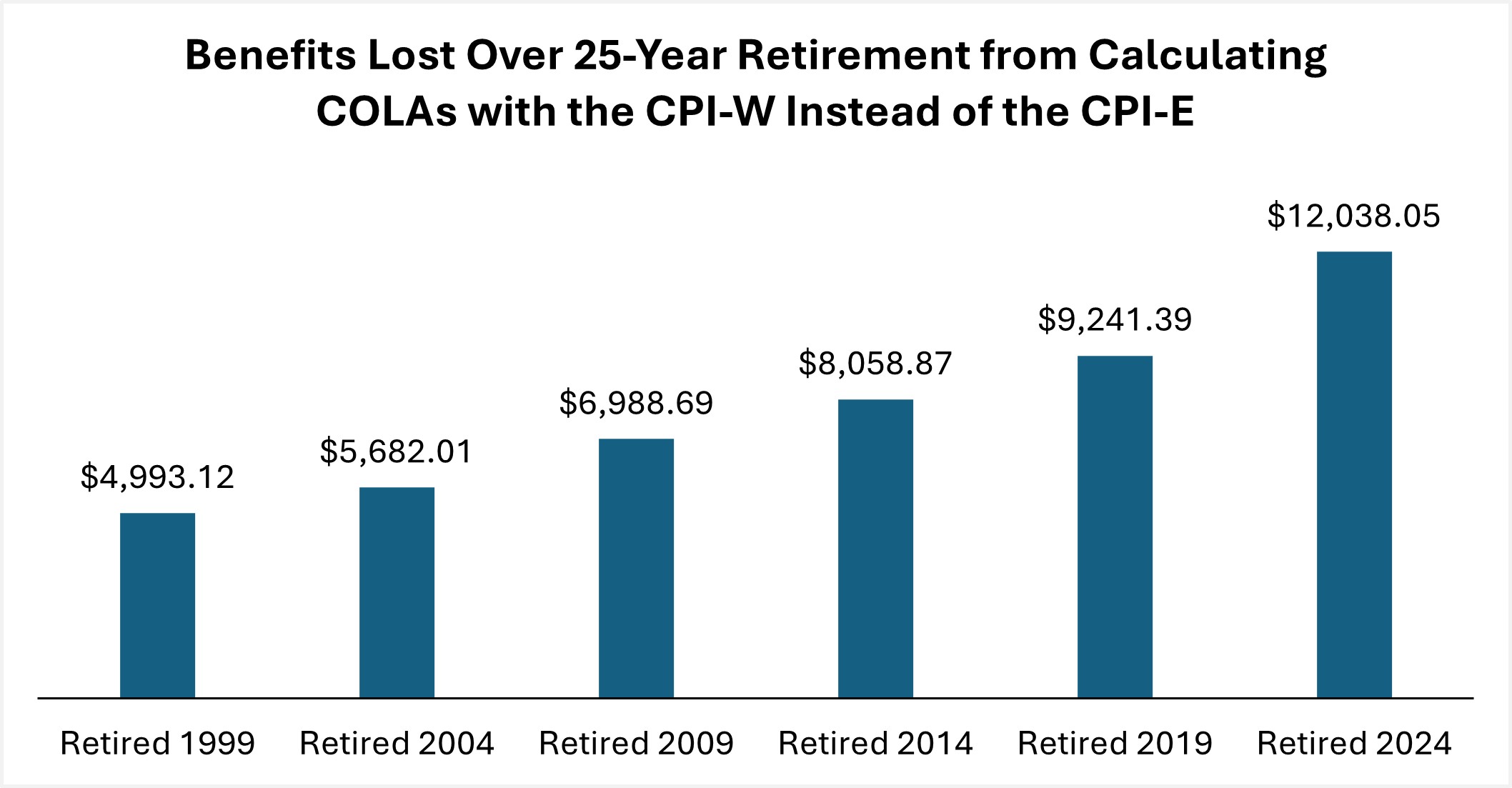

Social Security’s 2026 Cost-of-Living Announcement (COLA) has been delayed to Friday, October 24th, due to complications arising from the government shutdown. The announcement had previously been scheduled for today, October 15th. A new analysis from TSCL shows the average senior who retired in 1999 has lost nearly $5,000 in Social Security payments as a result of the government using the wrong price index to calculate Cost-of-Living Adjustments (COLAs). The COLA is currently calculated with the CPI-W, a price index that tracks inflation for people who work and live in cities. Instead, it should be using the CPI-E, which is designed to reflect seniors’ budgets and tends to come in slightly higher than the CPI-W. On average, the CPI-E comes in about 0.1 percentage points higher than the CPI-W. The cost of using the wrong price index is rising for seniors over time. As shown in the figure below, TSCL’s analysis predicts that, if current long-term inflation patterns continue, the average person who retired in 2014 will lose about $8,000 of benefits across a 25-year retirement from using COLAs calculated with the CPI-W instead of the CPI-E. For someone who retired in 2024, we project that number to rise to just over $12,000.

Key Insights:

The cost of using the wrong price index is rising for seniors over time. As shown in the figure below, TSCL’s analysis predicts that, if current long-term inflation patterns continue, the average person who retired in 2014 will lose about $8,000 of benefits across a 25-year retirement from using COLAs calculated with the CPI-W instead of the CPI-E. For someone who retired in 2024, we project that number to rise to just over $12,000.

Key Insights:

- The CPI-E has outperformed the CPI-W 69 percent of the time across the last 25 COLAs. On average, the CPI-E comes in at 2.7 percent, while the average CPI-W comes in at 2.6 percent. The CPI-E puts more emphasis on areas where seniors tend to spend more of their budget than younger Americans, such as housing and medical care.

- Congress has introduced bills to change the COLA calculation to the CPI-E, but they keep getting bogged down in D.C. gridlock. Examples include the Social Security Expansion Act (2025), the Boosting Benefits and COLAs for Seniors Act (2024), the Social Security 2100 Act (2023), and the Fair COLAs for Seniors Act (2023). None of the bills have passed into law.

- Changing to the CPI-E would bring relief to millions of seniors. TSCL’s 2025 Senior Survey estimates that approximately 21.8 million seniors, or 39 percent of Americans older than 65, depend on Social Security for 100 percent of their income. That study also finds the median senior gets by on less than $2,000 per month, with an estimated 7.3 million surviving on less than $1,000 per month. Meanwhile, the average rent for a 1-bedroom apartment was $1,550 as of the end of September, according to Zillow.

- “Continuing to calculate COLAs with the CPI-W when the CPI-E is already available is a great example of how Congress refuses to make even small changes that would benefit seniors. It’s not as if switching to the CPI-E would involve setting up some new metric. It already exists, and by definition, it’s better for American seniors.”

- “If Congress continues to pass the buck on switching to the CPI-E, the problem is only going to get worse and worse. Current retirees’ Social Security benefits will fall further behind inflation, while future retirees won’t just fall behind—they’ll start from the back.”

- “Seniors are tired of hearing that ‘no cuts’ is the best the government can offer them on Social Security. Our research shows that 93 percent of older Americans believe Social Security reform should be a high priority or top priority for the Trump Administration and Congress. They’re telling us they want change, and while switching to the CPI-E certainly won’t fix everything, at least it’s a start.”

- Shannon Benton, Executive Director: sbenton@tsclhq.org; 703-548-5568

- Alex Moore, Statistician: amoore@tsclhq.org; 571-374-2658