By Mary Johnson, Social Security and Medicare Policy Analyst

The Senior Citizens League’s (TSCL) latest study on Social Security Buying Power found that the average person who retired before 2000 (those age 85 and older) would need an extra $516.70 more per month ($6,200 in 2023) than he or she is currently getting just to maintain the same level of buying power as in 2000. In fact, Social Security benefits have lost 36% of their buying power since 2000.

Inflation is moderating, but a lower rate of inflation doesn’t necessarily mean that bills will slow down or that older households will see some improvement in household budgets, at least not right away. Our study confirms that the prices consumers pay simply aren’t growing as fast as a year ago. On the other hand, declining prices are pointing to a significantly lower Social Security cost-of-living adjustment (COLA) for next year of 3.1%.

In 2022, our Social Security Buying Power research, which compares how well COLAs keep pace with typical senior costs over time, found that Social Security benefits lost 40% of buying power since 2000. That was the deepest loss in buying power since the start of this study in 2010. This year, the study found that the loss of buying power moderated by 4 percentage points to 36%. But that is still one of the deepest losses recorded by this study, exceeded only by 2022.

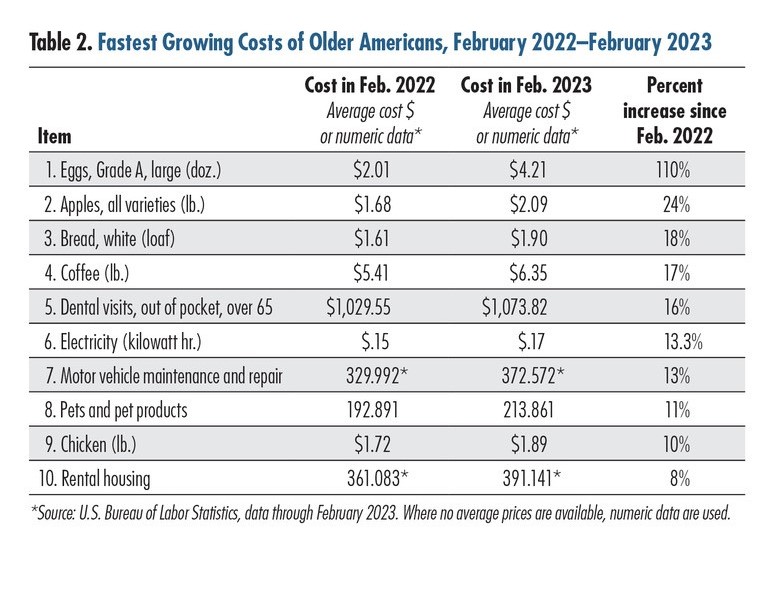

Our study compares the growth in the COLA since 2000 with increases in the price of 38 goods and services typically used by retirees over the same period. This year buying power was most impacted by the sharp increase in food items, electricity, rental housing, repair, maintenance of vehicles, and a stunning 16% increase in the cost of dental care. Topping our list of fastest-growing items? Eggs!

Our study examines expenditures that are typical for people ages 65 and up, comparing the growth in the prices of these goods and services to the growth in the annual COLAs. It includes cost increases in Medicare premiums and out–of–pocket health care costs that are not tracked under the consumer price index currently used to calculate the COLA – the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The study found that, since 2000, COLAs have increased Social Security benefits by a total of 78%, yet typical senior expenses through February of 2023 grew by 141.4%. The average Social Security benefit in 2000 was $816 per month. Due to COLA increases, that benefit grew to $1,453.20 by 2023. But because retiree costs are rising so much faster than the COLA, this study found that a Social Security benefit of $1,969.80 per month, $516.70 more per month than currently paid, would be required just to maintain the same level of buying power as in 2000. The following table illustrates the top ten fastest-growing costs for older consumers from March 2022 to February 2023.

Social Security benefits do not buy as much today as in 2000. For every $100 of goods or services that retirees bought in 2000, they could only buy $64 worth today.

TSCL supports four reforms to protect the buying power of Social Security benefits:

- Provide a modest boost to the benefits of all retirees, to better protect them from falling into poverty and to strengthen retirement income.

- Tie the annual COLA to a seniors’ consumer price index such as the Consumer Price Index for Elderly (CPI -E). This index tends to show inflation growing at a modestly faster rate than the CPI-W in many years.

- Guarantee a minimum COLA of no less than 3%. The guarantee is especially important in years when inflation goes negative, and no COLA is payable at all.

- Adjust the income thresholds that subject Social Security benefits to taxation for inflation to allow beneficiaries to keep more of their benefits.