Update: Social Security Benefits Lose 32 Percent of Buying Power

(Washington, DC) – Consumer price index data through August 2021 indicates that the 2022 COLA will likely be about 6 percent. But soaring inflation this year has deeply eroded the buying power of Social Security benefits, according to a new update to an ongoing inflation study by The Senior Citizens League (TSCL). The study, which compares the growth in the Social Security cost of living adjustments (COLA)s with increases in the costs of goods and services typically used by retirees found that, since 2000, Social Security benefits have lost 32 percent of their buying power.

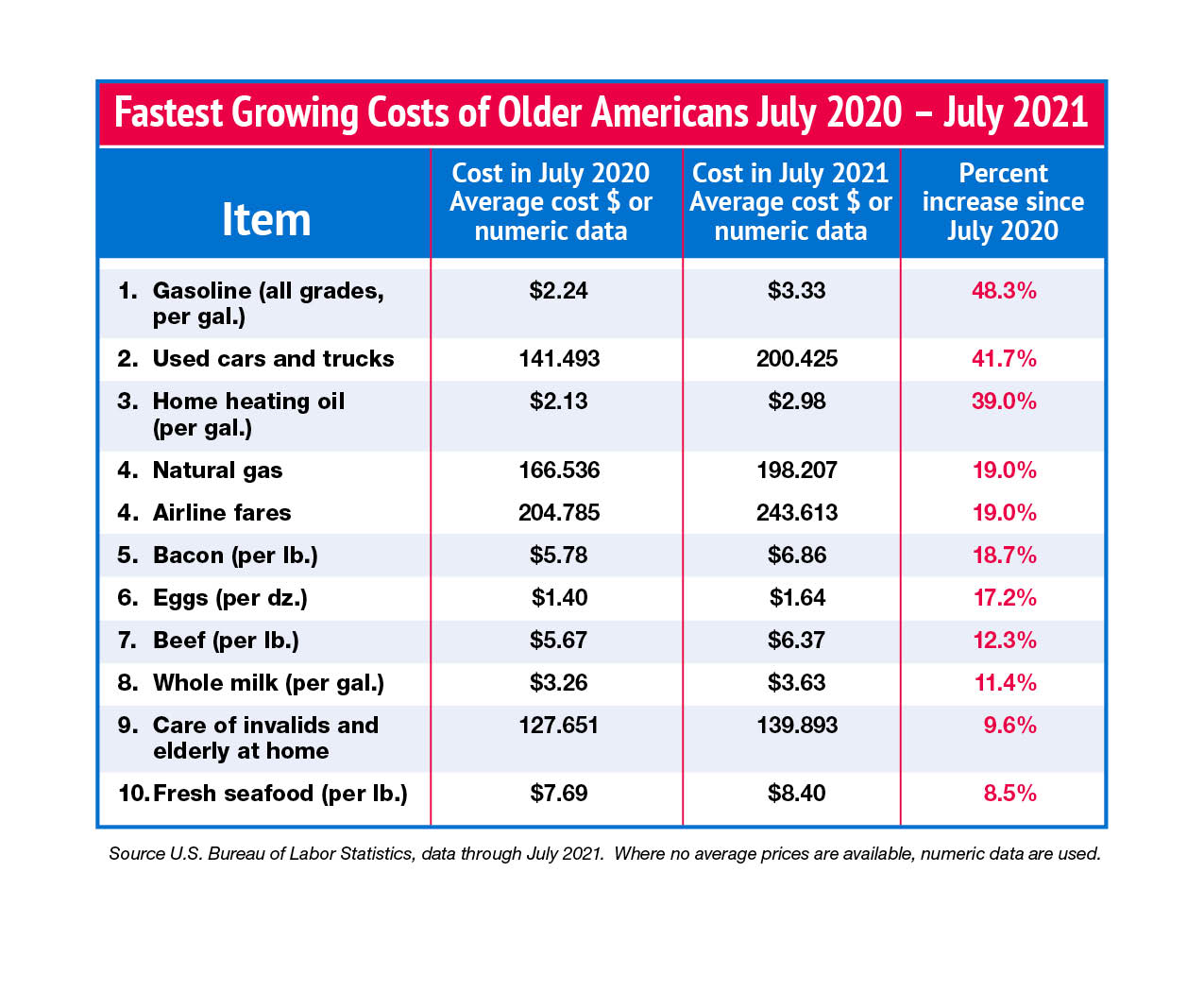

The annual COLA increased Social Security benefits in January of 2021 by just 1.3 percent. While mild inflation in 2020 did improve the buying power of Social Security benefits by 2 percentage points through the month of January 2021 — from a loss in buying power of 30 percent to a loss of 28 percent — that improvement was completely wiped out by soaring inflation in February and March of this year,” says Mary Johnson, a Social Security policy analyst for The Senior Citizens League (TSCL). Based on consumer price data through July 2021, the erosion in the buying power of Social Security benefits has deepened to 32 percent over the 21 – year period.

Social Security benefits are one of the few sources of retirement benefits to be adjusted for inflation. The intention is to protect the buying power of benefits when prices increase. But retirees frequently notice that over time their Social Security benefits don’t buy as much as they used to. This happens when the annual COLA doesn’t keep pace with the increases in costs typically experienced by older and disabled beneficiaries.

This study looks at 39 expenditures that are typical for people age 65 and up, comparing the growth in the prices of these goods and services to the growth in the annual COLAs. It includes cost increases in Medicare premiums and out of pocket costs that aren’t tracked under the index currently used to calculate the COLA.

Since 2000, COLAs have increased Social Security benefits a total of 55 percent, yet typical senior expenses through July 2021 grew 104.8%. The average Social Security benefit in 2000 was $816 per month. That benefit grew to $1,262.40 by 2021 due to COLA increases. However, because retiree costs are rising at a far more rapid pace than the COLA, this study found that a Social Security benefit of $1,671.20 per month ($408.80 more) would be required just to maintain the same level of buying power that $816 had in 2000.

“To put it in perspective, for every $100 worth of groceries a retiree could afford in 2000, they can only buy $68 worth today,” Johnson notes. To help protect the buying power of benefits, The Senior Citizens League supports legislation that would provide a modest boost in benefits and base COLAs on the Consumer Price Index for the Elderly (CPI-E) or guarantee a COLA no lower than 3 percent. In addition The League has recently launched a campaign for a $1,400 stimulus check to help Americans struggling to cope with high inflation. To learn more about these initiatives, visit www.SeniorsLeague.org.

###

With 1.2 million supporters, The Senior Citizens League is one of the nation’s largest nonpartisan seniors groups. Its mission is to promote and assist members and supporters, to educate and alert senior citizens about their rights and freedoms as U.S. Citizens, and to protect and defend the benefits senior citizens have earned and paid for. The Senior Citizens League is a proud affiliate of The Retired Enlisted Association. Visit www.SeniorsLeague.org for more information.

ALSO AVAILABLE TO JOURNALISTS: Social Security Loss of Buying Power report including study methodology available for download. Loss of Buying Power Report.